About Me

Hi, I'm Rita.

I'm a Mortgage Professional with broad experience in all aspects of the financing process - whether it be helping first-time buyers purchase their first home; assisting clients with financing for a renovation to their existing home; building a new home or helping them re-negotiate their mortgage at renewal.

My goal is to help my clients navigate through the process of finding the right financing product for their unique situation.

I specialize in mortgages for self-employed borrowers; borrowers with slightly bruised credit and first time home buyers, home equity Lines of Credit; first & second mortgages; mortgage renewals; re-finances and investment property mortgages.

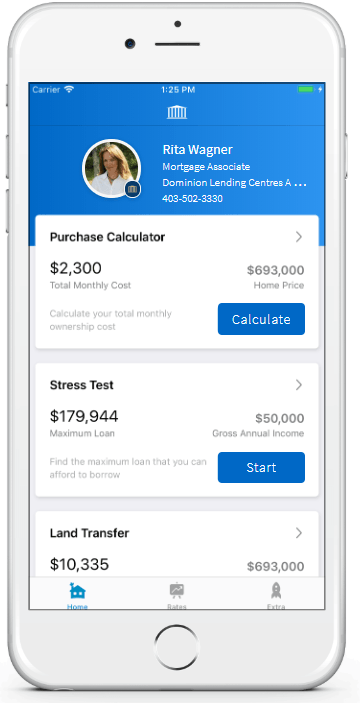

Cell: 403-502-3330

STEP ONE

Start the conversation.

The best place to start is to connect with me directly. The mortgage process is personal, and it can be daunting. My commitment to you is that I'll listen to all your needs, assess your financial situation, and provide you with a plan to move forward.

STEP TWO

Choose the best option.

Once we’ve had a look at your financial situation, we’ll consider a variety of mortgage options, I’ll outline what documents are necessary to qualify for a mortgage, negotiate with the lenders on your behalf, and arrange the mortgage that best suits your needs.

STEP THREE

Sit back and relax.

Once we’ve arranged the mortgage product that best suits your needs, you’re not alone. I’m your mortgage professional for life. If you’ve got questions in the years to come, I’m always available to make sure that your mortgage is working for you, and not the other way around!

Lenders

I've developed excellent relationships with many lenders across the country.

Let's figure out which one has the best product for you.

Services

As a mortgage professional it's my job to be the go-between between you and a mortgage lender. I make sure that you know all the products available to you, and are equipped with the knowledge to make the best decisions for you and your family.

Flexible Mortgages

As your life can change at any time, I offer a wide range of flexible mortgage products.

Qualified Advice

As a licensed mortgage expert, I'll listen to your needs and answer your questions.

No Cost to You

There are no fees for my services, once you find the perfect product, the lender pays me a commission.

Advocacy

I commit to working on your behalf

to find you the best mortgage for your needs.

Mortgage Articles

Can You Afford That Mortgage? Let’s Talk About Debt Service Ratios One of the biggest factors lenders look at when deciding whether you qualify for a mortgage is something called your debt service ratios. It’s a financial check-up to make sure you can handle the payments—not just for your new home, but for everything else you owe as well. If you’d rather skip the math and have someone walk through this with you, that’s what I’m here for. But if you like to understand how things work behind the scenes, keep reading. We’re going to break down what these ratios are, how to calculate them, and why they matter when it comes to getting approved. What Are Debt Service Ratios? Debt service ratios measure your ability to manage your financial obligations based on your income. There are two key ratios lenders care about: Gross Debt Service (GDS) This looks at the percentage of your income that would go toward housing expenses only. 2. Total Debt Service (TDS) This includes your housing costs plus all other debt payments—car loans, credit cards, student loans, support payments, etc. How to Calculate GDS and TDS Let’s break down the formulas. GDS Formula: (P + I + T + H + Condo Fees*) ÷ Gross Monthly Income Where: P = Principal I = Interest T = Property Taxes H = Heat Condo fees are usually calculated at 50% of the total amount TDS Formula: (GDS + Monthly Debt Payments) ÷ Gross Monthly Income These ratios tell lenders if your budget is already stretched too thin—or if you’ve got room to safely take on a mortgage. How High Is Too High? Most lenders follow maximum thresholds, especially for insured (high-ratio) mortgages. As of now, those limits are typically: GDS: Max 39% TDS: Max 44% Go above those numbers and your application could be declined, regardless of how confident you feel about your ability to manage the payments. Real-World Example Let’s say you’re earning $90,000 a year, or $7,500 a month. You find a home you love, and the monthly housing costs (mortgage payment, property tax, heat) total $1,700/month. GDS = $1,700 ÷ $7,500 = 22.7% You’re well under the 39% cap—so far, so good. Now factor in your other monthly obligations: Car loan: $300 Child support: $500 Credit card/line of credit payments: $700 Total other debt = $1,500/month Now add that to the $1,700 in housing costs: TDS = $3,200 ÷ $7,500 = 42.7% Uh oh. Even though your GDS looks great, your TDS is just over the 42% limit. That could put your mortgage approval at risk—even if you’re paying similar or higher rent now. What Can You Do? In cases like this, small adjustments can make a big difference: Consolidate or restructure your debts to lower monthly payments Reallocate part of your down payment to reduce high-interest debt Add a co-applicant to increase qualifying income Wait and build savings or credit strength before applying This is where working with an experienced mortgage professional pays off. We can look at your entire financial picture and help you make strategic moves to qualify confidently. Don’t Leave It to Chance Everyone’s situation is different, and debt service ratios aren’t something you want to guess at. The earlier you start the conversation, the more time you’ll have to improve your numbers and boost your chances of approval. If you're wondering how much home you can afford—or want help analyzing your own GDS and TDS—let’s connect. I’d be happy to walk through your numbers and help you build a solid mortgage strategy.

Wondering If Now’s the Right Time to Buy a Home? Start With These Questions Instead. Whether you're looking to buy your first home, move into something bigger, downsize, or find that perfect place to retire, it’s normal to feel unsure—especially with all the noise in the news about the economy and the housing market. The truth is, even in the most stable times, predicting the “perfect” time to buy a home is incredibly hard. The market will always have its ups and downs, and the headlines will never give you the full story. So instead of trying to time the market, here’s a different approach: Focus on your personal readiness—because that’s what truly matters. Here are some key questions to reflect on that can help bring clarity: Would owning a home right now put me in a stronger financial position in the long run? Can I comfortably afford a mortgage while maintaining the lifestyle I want? Is my job or income stable enough to support a new home? Do I have enough saved for a down payment, closing costs, and a little buffer? How long do I plan to stay in the property? If I had to sell earlier than planned, would I be financially okay? Will buying a home now support my long-term goals? Am I ready because I want to buy, or because I feel pressure to act quickly? Am I hesitating because of market fears, or do I have legitimate concerns? These are personal questions, not market ones—and that’s the point. The economy might change tomorrow, but your answers today can guide you toward a decision that actually fits your life. Here’s How I Can Help Buying a home doesn’t have to be stressful when you have a plan and someone to guide you through it. If you want to explore your options, talk through your goals, or just get a better sense of what’s possible, I’m here to help. The best place to start? A mortgage pre-approval . It’s free, it doesn’t lock you into anything, and it gives you a clear picture of what you can afford—so you can move forward with confidence, whether that means buying now or waiting. You don’t have to figure this out alone. If you’re curious, let’s talk. Together, we can map out a homebuying plan that works for you.

If you’ve been thinking about buying a property, whether that be your first home, next home, forever home, or a home to retire into, the current state of the Canadian economy might have you wondering: Is this really the right time to make a move? There is certainly no shortage of doom and gloom in the news out there. The truth is, that’s a tough question to answer in the best of times. It’s nearly impossible to know for sure what’s going to happen next with the housing market in Canada. It could heat up or it could cool down. So here’s some advice. Instead of basing your buying decision entirely on external market factors, like the economy or housing market, consider looking for the answers internally. When you stop looking at the market to determine your timing to buy a home, and instead examine the personal reasons you have for wanting to buy a home, the picture can become much clearer. Here are some questions to consider. Although they are subjective, they will help bring you clarity. Ask yourself: Does buying a property now put me in a better financial position? Do I make enough money now to afford a new home and maintain my lifestyle? Do I feel confident with my current employment status? Have I saved enough money for a down payment? How long do I plan on living in this new home? Is there any scenario where I might have to sell quickly and potentially lose money? Does buying a property now move me closer to my life goals? Do I really want to buy now or am I just feeling a lot of pressure to just buy something? Am I holding back because I'm scared property prices might drop soon? There’s no doubt that buying a home can be stressful, but it doesn’t have to be. Having a plan in place is the best course of action to help you make good decisions and alleviate that stress. If you’d like to have a conversation to discuss your plans, ask some questions, and map out what buying a home looks like for you, we can address many of the unknowns together. The best place to start is to work through a mortgage pre-approval. There is no cost for this service, you’ll learn exactly what you can qualify for, and it will provide a lot of clarity about your situation. You might decide that it’s best to wait before buying, and that’s just fine. You might find that now’s a perfect time for you to buy! If you'd like to talk, please connect anytime. You’re not in this alone. We can work through everything together.

Nice things people have said about working with me.

Let's Run Some Numbers

Download My Mortgage Toolbox

WHAT CAN YOU DO WITH MY APP

- Calculate your total cost of owning a home

- Estimate the minimum down payment you need

- Calculate Land transfer taxes and the available rebates

- Calculate the maximum loan you can borrow

- Stress test your mortgage

- Estimate your Closing costs

- Compare your options side by side

- Search for the best mortgage rates

- Email Summary reports (PDF)

- Use my app in English, French, Spanish, Hindi and Chinese